Market Monitor | January Update

Headlines and Highlights

- Kevin Warsh tapped for Fed chair: After months of reality-show-like drama, President Trump has nominated former Federal Reserve governor Kevin Warsh to be the next chair of the central bank. If approved by the Senate, Warsh would succeed Jerome Powell, whose term expires in May. Among the front runners from the start, Warsh is widely viewed as a moderate choice given his long experience as a Wall Street banker and his years as a Fed governor (2006-2011). The dollar immediately strengthened and the price of gold and crypto plummeted after his selection was announced as Warsh is viewed as ‘hawkish’ by prioritizing keeping inflation low. But as Fed chair, he will likely feel White House pressure to cut short-term interest rates to stoke economic growth ahead of the 2026 midterm elections.

- Fed stands pat at January meeting: The Federal Open Market Committee met expectations at its late January meeting by keeping short-term interest rates at 3.5% to 3.75%. The no-action decision broke a streak of three straight meetings at which the panel reduced the federal funds rate by a quarter of a percentage point. Fed Chair Powell cited stronger-than-anticipated economic activity and signs of a stabilizing jobs market as the key reasons for holding rates steady. The Fed’s internal forecasting indicates a single rate cut in 2026, while the futures market currently envisions two cuts – the first in June, after Powell’s term ends, and the second in the fall.

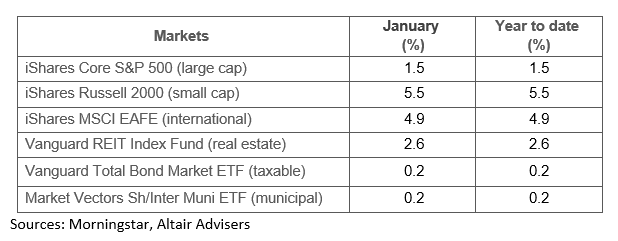

- Fast start for small caps, international: S. small-cap and international stocks are off to a strong start in 2026, powered respectively by the prospects of more interest rate cuts and a furthering weakening of the dollar. Small caps as measured by the iShares Russell 2000 ETF increased 5.5% during the month, while the iShares MSCI EAFE ETF of non-U.S. developed-market stocks was up 4.9%. Both had been higher but gave back some of their gains after the Warsh nomination for Fed chair tempered rate and currency expectations. U.S. large caps picked up 1.5% in January. The Vanguard REIT Index rose 2.6% on the interest-rate outlook and strength in the data center and health care sectors. The bond market was essentially flat.

Select Market Returns

Our Views

- The choice of Kevin Warsh as the next Fed chair is a sensible pick given the other contenders. His past experience on Wall Street and at the Fed positions him as a traditionalist, which eases some worries about future interest-rate policy and Fed independence.

- We envision at least two rate cuts by the Federal Reserve this year to support the softening labor market. Inflation is above the Fed’s target but it appears stable, making the benefits of supporting job creation more important now than the potential risk of too much monetary stimulus.

- The fast start for international stocks in 2026 aligns with our view that conditions are promising for non-U.S. developed and emerging markets (the latter of which posted an 8% gain in January). The key drivers for these markets are stronger earnings growth and a weaker dollar.

- U.S. small caps dipped in late January on expectations that interest-rate cuts may not come as quickly under Warsh at the Fed compared to other leading candidates. But rates are still likely heading down and projected earnings are heading up – both are good for small caps.

- The AI growth story is still expected to be one of the largest contributors to U.S. stock performance this year, but it is not the only story. Forecasts of rising revenue and earnings growth for most of the S&P 500 sectors should be another important contributor.

The material shown is for informational purposes only. Past performance is not indicative of future performance, and all investments are subject to the risk of loss. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties and actual results may differ materially from those anticipated in forward-looking statements. As a practical matter, no entity is able to accurately and consistently predict future market activities. Information herein incorporates Altair Advisers’ opinions as of the date of this publication, is subject to change without notice, and should not be considered as a solicitation to buy or sell any security. While efforts are made to ensure information contained herein is accurate, Altair Advisers cannot guarantee the accuracy of all such information presented. Material contained in this publication should not be construed as accounting, legal, or tax advice. See Altair Advisers’ Form ADV Part 2A and Form CRS at https://altairadvisers.com/disclosures/ for additional information about Altair Advisers’ business practices and conflicts identified. All registered investment advisers are subject to the same fiduciary duty as Altair Advisers.