October 3, 2023

Market Monitor: September Update

Headlines and Highlights

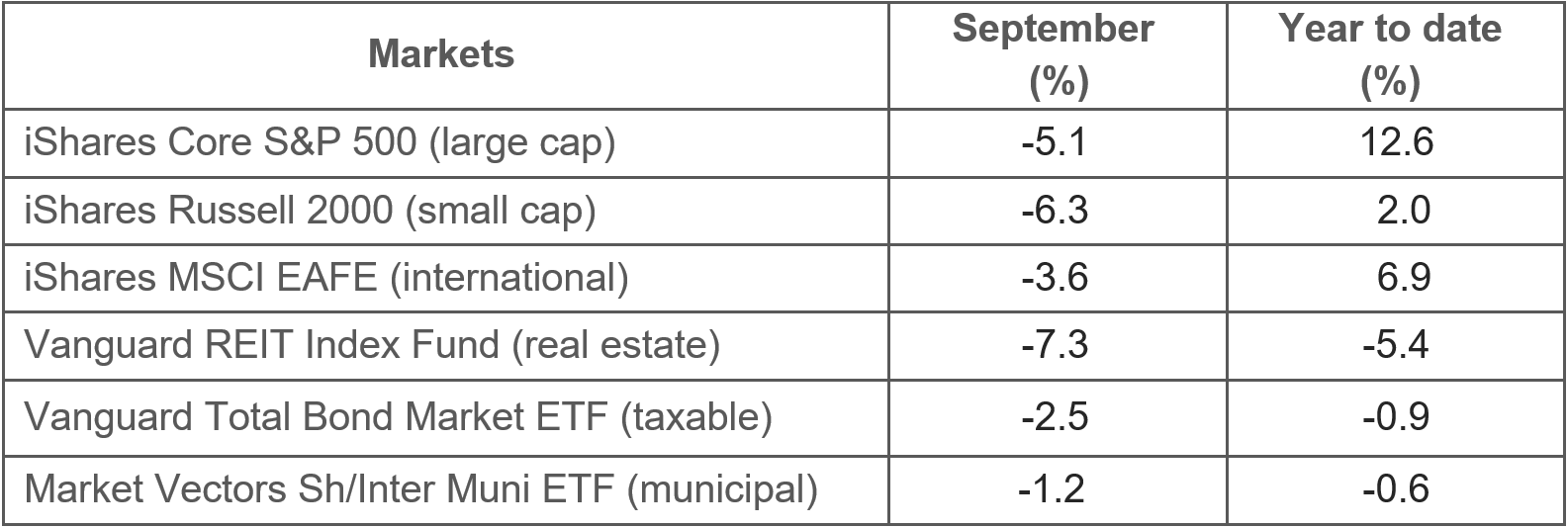

- Markets endure worst month of 2023: Stocks and bonds both saw their biggest monthly declines of the year in September, climaxing a quarter that was negative across most asset classes. Surging bond yields, rising oil prices and concerns that persistently high interest rates could erode the economy’s resilience combined to heighten investor pessimism. U.S. stocks as benchmarked by the S&P 500 Index retained a 12.6% year-to-date gain despite falling 5.1% for the month and 3.7% for the quarter. Bonds had their worst month since September 2022 as the 10-year Treasury yield climbed to 4.6%, sending prices of existing bonds lower.

- Government shutdown averted: Congress passed a temporary stopgap extension of federal funding with just hours to spare before the end of the fiscal year on September 30th, keeping government operations functioning normally until November 17th. With House Speaker Kevin McCarthy facing a challenge to his position from within Republican ranks, it remains unclear whether the next deadline will involve a similar last-minute showdown.

- Inflation outlook brightens: Underlying inflation fell below an annual rate of 4% for the first time in over two years, an encouraging sign for the Federal Reserve as it determines whether to stop raising interest rates. The core personal consumption expenditures price index, which strips out the volatile food and energy components, was up 3.9% year-over-year in August after climbing just 0.1% for the month.

Selected Market Returns

Sources: Morningstar, Altair Advisers

Our Views

- The economy got a welcome reprieve from the eleventh-hour agreement heading off a government shutdown at a time it already is under pressure from high interest rates, above-average inflation and higher energy prices. A shutdown remains a possibility after the 45-day stopgap funding expires, but a major impact on markets is unlikely if one happens. More than 20 such shutdowns have occurred in the last 50 years and they have had little lasting impact on growth, stocks or bonds.

- Consumer confidence and sentiment both weakened in September, according to separate gauges – a cautionary sign for the U.S. economy if the trend continues. A moderation in consumer spending, the main engine of the economy, has helped reduce inflation. But a significant decline, if one were to occur, would be cause for concern.

- Federal Reserve officials have repeatedly cited the possibility of one more interest-rate hike this year. However, we view this as precautionary rhetoric in case inflation data worsens materially. We believe the Fed is likely to keep rates at the current 5.25% level well into next year.

- Inflation is cooling in the U.S. and Europe but remains high by historical standards despite central banks’ persistent monetary tightening. We expect it to continue slowing for the rest of the year. If it remains sticky into next year, hopes of a soft landing for the economy would be in jeopardy.

- Corporate earnings appear to be improving in the second half of 2023 but the slow pace of improvement reflects the challenging environment that companies face. FactSet forecasts that third-quarter profits will be 0.1% below the same period a year ago, which would be the smallest quarterly decline in a year but still negative. We will be closely watching upcoming earnings results and guidance as important indicators of the economy’s strength.

The material shown is for informational purposes only. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties, and actual results may differ materially from those anticipated in forward-looking statements. As a practical matter, no entity is able to accurately and consistently predict future market activities, and all investments are subject to the risk of loss. While efforts are made to ensure information contained herein is accurate, Altair Advisers LLC cannot guarantee the accuracy of all such information presented. Material contained in this publication should not be construed as accounting, legal, or tax advice