June Update

Headlines & Highlights

- U.S., Iran negotiating peace details: Representatives for the United States and Iran returned to Qatar in late June to start mediated talks on implementing the peace proposal that both sides signed earlier in the month. This comes a few days after a brief exchange of airstrikes in the Strait of Hormuz that disrupted ship traffic and raised some doubts about whether the tentative deal will be finalized. Even with the disruption, oil tankers have been moving through the strait at the fastest pace since the war began in late February – this supply boost has helped drive down the global price of crude from $83 to $71 per barrel since mid-June.

- Inflation reading highest since 2023: Elevated energy prices helped push the Federal Reserve’s preferred measure of inflation to its highest level in more than three years. The Personal Consumption Expenditures (PCE) deflator rose to an annual rate of 4.1% in May, up from 3.8% in the previous month and the highest since April 2023. Costlier gasoline and personal computers were among the factors cited as key contributors to the inflation increase. Gas prices have come down since the Iran War peace framework was signed, but at the end of June, the national average for a gallon of regular was $3.85, compared to just under $3.20 a year earlier.

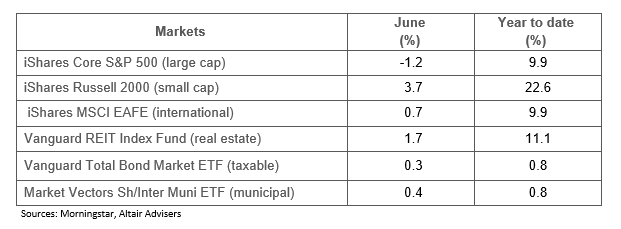

- Stocks post stellar results in Q2: The S&P 500 gained 15.0% in the second quarter of 2026, its best quarter since the Q2 2020 rebound from the pandemic-related market collapse. The strong quarterly performance, sparked by accelerating earnings growth and increased optimism for Middle East peace, lifted the large-cap index back into positive territory for the year (9.9%). Other equity asset classes fared even better in the latest quarter, with U.S. small caps rising 21.4% (22.6% year to date) and emerging-market shares picking up 21.1% (25.7% YTD). International developed markets turned in a more-than-respectable 8.6% in the quarter (9.9% YTD). Real-estate investment trusts (REITs) rose 9.7% in Q2 (11.1% YTD), led by the rapid expansion of data centers.

Select Market Returns

Our Views

- The Iran War has lasted longer than we originally expected, but the ceasefire in place since early April has largely limited active hostilities between the U.S. and Iran. Our early view – both sides have more reasons to settle than to keep fighting – remains valid and it is why we still believe a final peace deal will eventually be reached via negotiations.

- A more normalized flow of Middle East oil and other commodities out of the Persian Gulf may bring down headline inflation fairly quickly. A retreat in core inflation, which excludes volatile food and energy, will take longer because many consumer businesses that have raised prices to cover their higher costs tend to lower them more slowly.

- New Fed chair Kevin Warsh said the central bank’s top priority is to get inflation back down to its target rate of 2%, a level not seen in the U.S. since February 2021. The market has interpreted Warsh’s words to mean short-term interest rates will be heading up this year, but we believe easing inflationary pressures will enable the Fed to hold rates steady.

- U.S. economic growth in the first quarter of 2026 was stronger than previously expected – the Bureau of Economic Analysis upgraded real GDP growth for the period to an annualized rate of 2.1%, up from 1.6% in its initial estimate. We expect growth to remain solid, with lower energy prices and the ongoing AI infrastructure buildout providing momentum.

- S&P 500 earnings expectations for the second quarter continue to head higher – the latest estimate from the data firm FactSet calls for a 23.1% earnings jump in Q2 compared to the same period in 2025. With energy (+123%) and technology (+63%) leading the way in earnings growth, 10 of the 11 S&P 500 sectors are on track to grow their profits in Q2.

The material shown is for informational purposes only. Past performance is not indicative of future performance, and all investments are subject to the risk of loss. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties and actual results may differ materially from those anticipated in forward-looking statements. As a practical matter, no entity is able to accurately and consistently predict future market activities. Information herein incorporates Altair Advisers’ opinions as of the date of this publication, is subject to change without notice, and should not be considered as a solicitation to buy or sell any security. While efforts are made to ensure information contained herein is accurate, Altair Advisers cannot guarantee the accuracy of all such information presented. Material contained in this publication should not be construed as accounting, legal, or tax advice. See Altair Advisers’ Form ADV Part 2A and Form CRS at https://altairadvisers.com/disclosures/for additional information about Altair Advisers’ business practices and conflicts identified. All registered investment advisers are subject to the same fiduciary duty as Altair Advisers.