Mid-Month Update

Headlines & Highlights

- U.S., Iran swapping peace proposals: The U.S.and Iran continue to trade peace proposals, but news reports indicate that the sides are still far apart in their efforts to negotiate an end to the conflict in the Persian Gulf region that started nearly three months ago. The future of Iran’s nuclear weapons program and its claim of sovereignty over the Strait of Hormuz are among the biggest sticking points. Hundreds of oil tankers and other vessels are stranded in the gulf due to Iran’s throttling of traffic. After a brief dip in early May, crude oil prices rose back over $106 per barrel; regular gasoline in the U.S. averaged $4.50 a gallon at mid-month.

- Inflation hits three-year high: Consumer prices in April were 3.8% higher than in the same month a year ago, the federal Bureau of Labor Statistics reported. The year-over-year increase in the Consumer Price Index was the largest since May 2023. Much of the April increase was due to higher fuel prices resulting from the Iran War – on average, gasoline in the U.S. is now roughly 50% more expensive than before the war started. So-called “core” inflation, which excludes food and energy, was 2.8% in April, up slightly from the previous month. Concern about accelerating inflation has driven bond yields sharply higher: The 10-year Treasury yield was 4.6%, its highest in a year, while the 30-year Treasury’s yield topped 5% for the first time since 2007. Bond prices move inversely to yields.

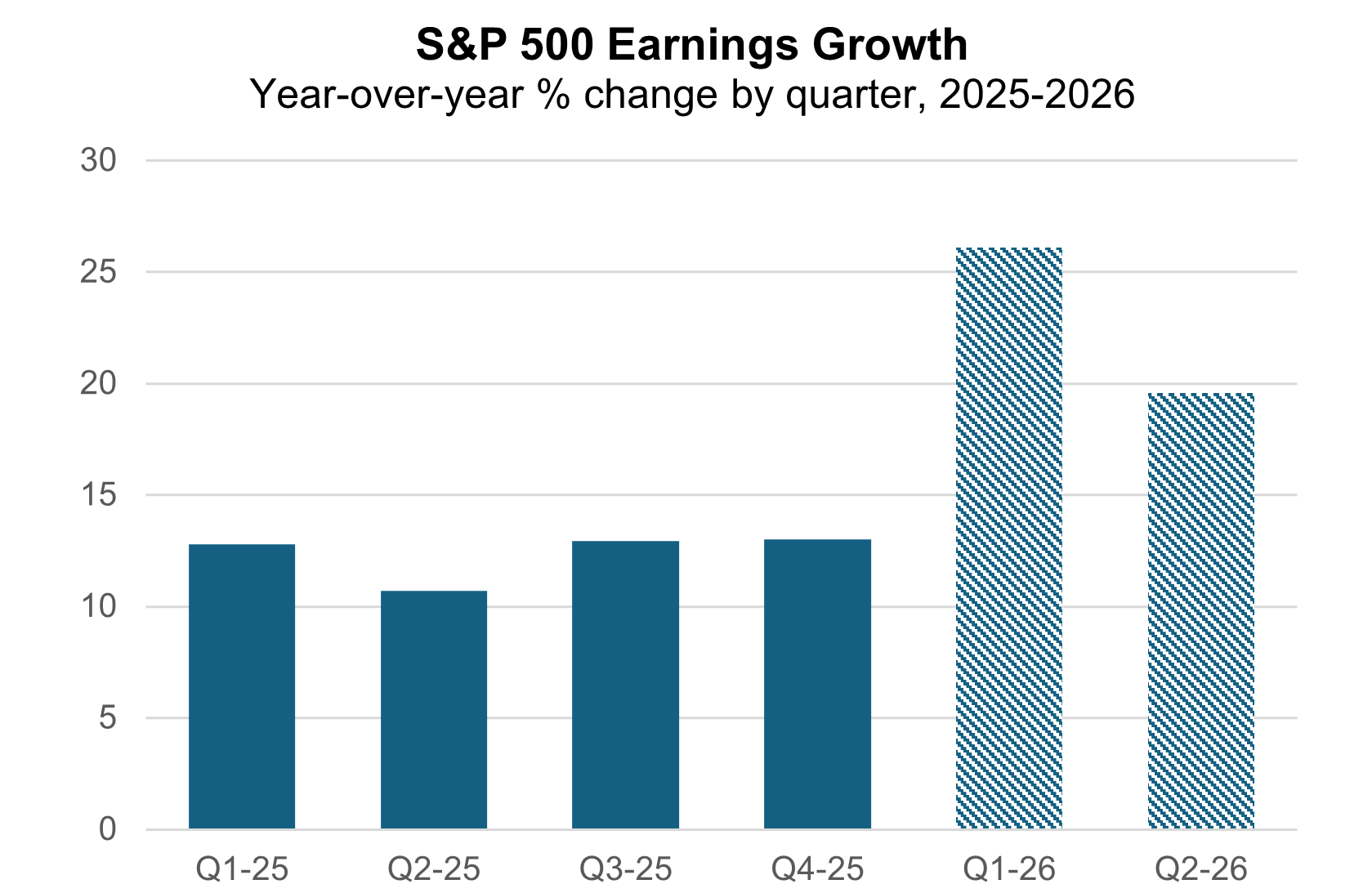

- U.S. stocks rise on stellar numbers: Upward earnings-growth revisions for 2026 pushed U.S. large-cap stocks to new records – the S&P 500 Index surpassed the 7,500 mark for the first time on May 14. The index has posted seven straight weeks of gains. With first-quarter results in for nearly all S&P 500 companies, year-over-year earnings growth stood at 26.1%, according to FactSet (see chart below). The benchmark ETF for U.S. large caps gained 2.8% in the first half of May (+8.7% year to date). U.S. small caps were down slightly so far in May on fears that interest rates will be hiked to combat inflation, but are still solid for the year – the benchmark ETF was up 12.9% YTD. Emerging markets continue to power forward, posting a 2.5% gain as of mid-month (18.9% YTD) while international developed markets dipped (+6.5% YTD).

Chart of Interest

20%+ growth for the rest of 2026 is pushing the S&P 500 higher.

Source: FactSet, Altair Advisers; Shaded bars indicate estimates as of May 15, 2026

Key Takeaways

- President Trump’s meetings with Chinese President Xi Jinping covered a range of topics but did not produce much in the way of specific agreements, including on the Iran war. China is the biggest customer for Iranian oil, buying 80% to 90% of the country’s output, but Beijing gave little indication that it might assume a greater role in trying to end the war.

- The Iran War ceasefire that went into effect on April 8 is still holding even as President Trump threatens that the U.S. could resume attacks on Iran at “a moment’s notice” if a peace deal is not reached soon. Iran says it will respond aggressively to any new attacks. An end to the ceasefire would likely push energy prices even higher and negatively affect equity and bond markets.

- Kevin Warsh was confirmed by the Senate to become the next head of the Federal Reserve – the 54-45 vote approving Warsh as the new Fed chair was the closest in the central bank’s history. President Trump picked Warsh to succeed Jerome Powell with expectations that he would move quickly to lower short-term interest rates, but accelerating inflation and a divided Fed may make that difficult.

- U.S. wholesale inflation for April was pushed higher by the war-related spike in energy prices, but the impact was even greater than for consumers. The Producer Price Index (PPI) jumped 6% from the April 2025 level, according to the Bureau of Labor Statistics. It was the fastest pace for price increases since 2022. The PPI reading adds support to the view that the Fed will hold off on interest-rate cuts.

- For full-year 2026, FactSet’s current projection is that earnings will be 22% higher than in 2025. In January, their full-year forecast was 12.8% annual earnings growth. The upswing in AI infrastructure outlays and resilient consumer spending despite higher prices are the key drivers of the positive trend. FactSet’s current prediction is 10.4% revenue growth in 2026, up from 7.2% in January.

The material shown is for informational purposes only. Past performance is not indicative of future performance, and all investments are subject to the risk of loss. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties and actual results may differ materially from those anticipated in forward-looking statements. As a practical matter, no entity is able to accurately and consistently predict future market activities. Information herein incorporates Altair Advisers’ opinions as of the date of this publication, is subject to change without notice, and should not be considered as a solicitation to buy or sell any security. While efforts are made to ensure information contained herein is accurate, Altair Advisers cannot guarantee the accuracy of all such information presented. Material contained in this publication should not be construed as accounting, legal, or tax advice. See Altair Advisers’ Form ADV Part 2A and Form CRS at https://altairadvisers.com/disclosures/for additional information about Altair Advisers’ business practices and conflicts identified. All registered investment advisers are subject to the same fiduciary duty as Altair Advisers.